The 4 Phases Where Dental Revenue Goes Missing

Revenue Leakage Audit Worksheet

Download the complete audit worksheet with benchmarks to find the $25K-$50K your practice loses annually.

Money does not just disappear. It leaks at specific, predictable points in your revenue cycle. Find the leaks and you find the lost revenue.

📚 Part of our reconciliation series: This article is part of The Complete Guide to Dental Practice Reconciliation, our comprehensive resource on closing your books accurately and preventing revenue leakage.

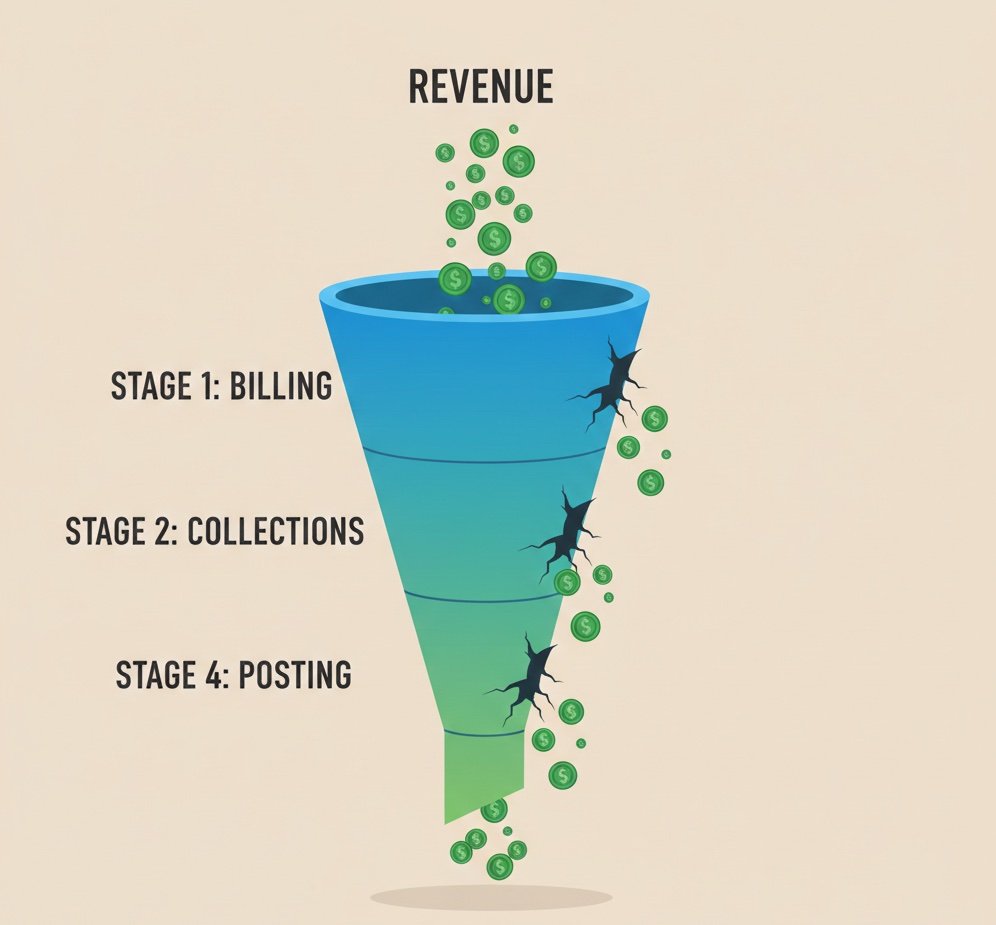

The Revenue Journey

Every dollar your dental practice earns travels through a journey from the moment it is owed to the moment it is verified in your accounts. Along this journey, there are four distinct phases where revenue can go missing.

Understanding these phases helps you identify where your practice is vulnerable. Most practices have strong controls in some phases and weak controls in others. The weak points are where money disappears.

This framework of Received, Recorded, Deposited, and Reconciled gives you a systematic way to evaluate your revenue cycle and find the gaps.

Phase 1: Received

The first phase is simply receiving the money. Before you can record, deposit, or reconcile anything, you have to actually collect payment.

Revenue leaks in the received phase when treatment is completed but never billed. Services get provided but claims never get submitted, which is especially common with secondary insurance not billed after primary pays, patient portions not collected at checkout, and insurance claims delayed until they are eventually forgotten.

Revenue also leaks when eligible payments are not collected. Patients leave without paying their portion. Insurance is not verified before appointments. Past-due balances are not collected when patients return for new visits.

Insurance denials accepted without question represent another leak. Claims that should be appealed get written off. Claims that need correction and resubmission get abandoned. Coordination of benefits issues go unresolved.

To find Phase 1 leaks, measure your collection rate by calculating net collection rate as collections divided by production minus contractual adjustments. Healthy practices collect ninety-six to ninety-eight percent. Below ninety-four percent indicates Phase 1 problems. Review denial rates by tracking claim denials and their outcomes. High denial rates without corresponding appeals suggest revenue left on the table.

Phase 2: Recorded

Once payment is received, it must be accurately recorded in your practice management system. This phase is where posting errors create problems.

Revenue leaks in the recorded phase when payments are posted to the wrong patient account. The money was collected but it is credited to someone other than the actual payer, creating confusion and potential duplicate billing.

Payments posted for wrong amounts represent another leak. Transposition errors, decimal point mistakes, and simple typos cause the recorded amount to differ from the actual payment received.

Payments not posted at all are a significant problem. Cash payments are especially vulnerable. Insurance payments can slip through when ERAs are not processed. Credit card payments sometimes miss posting when batch processing fails.

To find Phase 2 leaks, compare PMS payment totals to actual deposits. If your system shows more collected than was deposited, you have recording problems. Review patient account adjustments and look for patterns of corrections that suggest posting errors.

Phase 3: Deposited

Recorded payments must actually make it to the bank. This phase is where physical handling creates vulnerability.

Revenue leaks in the deposited phase when cash is skimmed before deposit. The payment is collected but some or all never reaches the bank account. This is theft and requires strong controls to prevent.

Checks can be lost or stolen between receipt and deposit. Without a restrictive endorsement stamp and proper tracking, checks are vulnerable during handling.

Deposits may be incomplete when not all collected payments are included in the bank deposit. Whether through error or intent, the deposit total differs from what should have been deposited.

To find Phase 3 leaks, compare PMS deposit records to bank deposits daily. The total your system shows for a deposit should match what the bank received exactly. Track the cash handling process end to end. Verify segregation of duties so the same person does not collect, post, and deposit.

Phase 4: Reconciled

The final phase is verification that what was received, recorded, and deposited all matches up and is properly reflected in your financial records.

Revenue leaks in the reconciled phase when variances are ignored rather than investigated. A difference exists between records but nobody researches why, and the discrepancy is simply written off.

Unidentified deposits accumulate when bank deposits cannot be traced to specific patient or insurance payments. The money is in the bank but you do not know where it came from.

Insurance payments are not matched to ERAs when deposits arrive without corresponding remittance information being processed. The money is deposited but not properly posted to patient accounts.

To find Phase 4 leaks, review your reconciliation process for thoroughness. Are all variances investigated or are some written off without research? Examine unidentified deposit balances. Any amount over a few hundred dollars represents Phase 4 failure.

Finding Your Weak Phase

Most practices are not equally vulnerable across all four phases. Identifying your weak phase helps you focus improvement efforts where they will have the most impact.

If collection rate is low but deposited amounts match PMS records, your problem is Phase 1. If PMS shows more collected than bank deposits, your problem is Phase 2 or 3. If bank deposits contain significant unidentified amounts, your problem is Phase 4.

Want to find where your revenue is leaking? Zeldent automatically reconciles across all four phases, matching PMS records to bank deposits and flagging discrepancies. Schedule a demo to see your revenue cycle clearly.

Revenue Leakage Audit Worksheet

Download the complete audit worksheet with benchmarks to find the $25K-$50K your practice loses annually.